News

Business and Market News Updates:

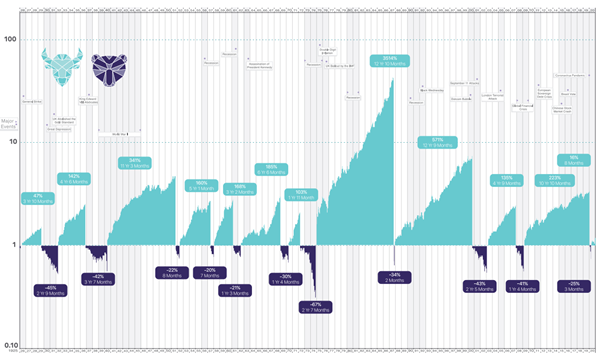

PWS Southport business news and market updates keeping you up to date on coronavirus news and how global stock markets are reacting to the ongoing pandemic.

Website Links

Where we have provided links to third party websites for further information, you should be aware that we are not responsible for the accuracy, availability or functionality of these sites, and thus cannot be held liable, directly or indirectly, for any loss however caused by your use of these linked sites.

As well as reviewing the operation of capital gains tax (CGT), the Chancellor asked the Office of Tax Simplification to consider “opportunities to simplify the tax”.

What changes could emerge and what could this mean for financial planning strategies for our clients?

Charging capital gains made by individuals to income tax

If you are taxed at the basic rate of tax on your total taxable income, you pay CGT at 10% (or 18% if the asset disposed of is a residential property) on any capital gains falling within the basic rate band.

If you have income taxable at the higher rate of 40% and/or the additional rate of 45% your capital gains are taxed at 20% (or 28% if the asset disposed of is a residential property).

Aligning these rates with income tax (20%/40%/45%) could double CGT for most taxpayers. This is not small change as CGT currently yields around £10 bn each year.

Such a change could make the use of investment bonds more attractive. Of course, this assumes that no consequential amendments are made to other parts of the tax code. And some suggest aligning CGT to income tax should be accompanied by the introduction of indexation relief.

Removing CGT “re-basing” on death

Currently, when someone holding an investment dies, the amount they paid for the investment “rebases” to the value at death. Getting rid of this has already been suggested by the OTS in their review of inheritance tax (IHT). This would be another negative change in relation to assets subject to CGT.

Further changes to entrepreneur’s relief (now known as business asset disposal relief).

business asset disposal relief is something you can claim as a way of minimising your tax when selling all or part of your business. It allows you to apply a reduced rate of 10% capital gains tax on the profits you make when you sell qualifying assets (such as your business).

Given the very recent reduction of the lifetime limit to £1m from £10m any further change may be unlikely.

A limitation of the annual exemption

The capital gains tax allowance in 2020-21 is £12,300. This is the amount of profit you can make from an asset this tax year before any CGT is payable.

Rather than removal, and especially if is aligned with income tax, then maybe a merger of the personal allowance and CGT annual exemption could happen.

The private residence exemption

Principal private residence (PPR) relief is a tax relief which protects an individual selling their home from capital gains tax on any gain. While its complete removal seems highly unlikely, some sort of cap (perhaps a cumulative lifetime cap) may be possible?

{kind=link}